The ESG Ratings Regulation imposes website disclosure obligations on UCITS managers and AIFMs that include ESG ratings in fund marketing communications.

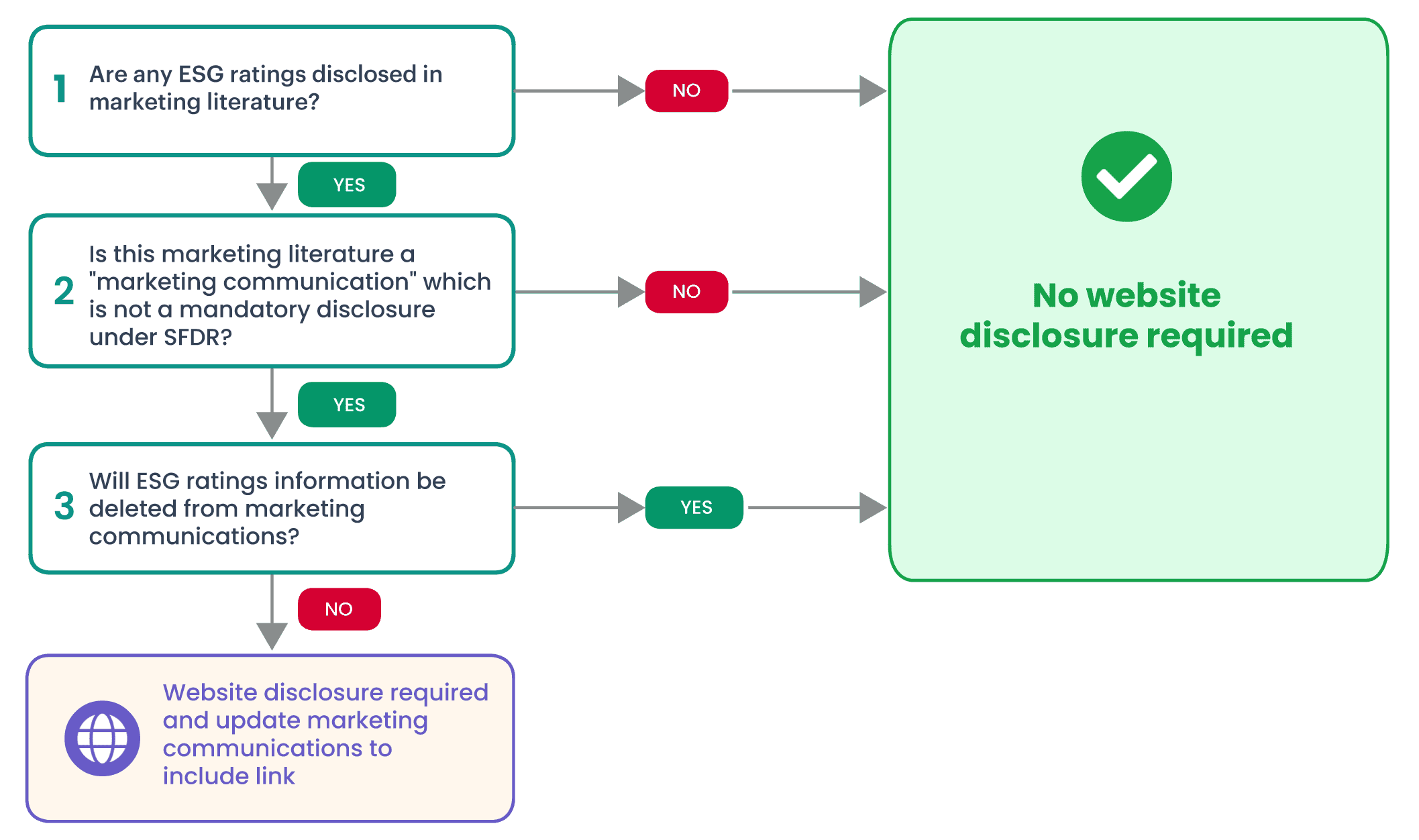

Where a fund manager, as part of its marketing communications for regulated products or services, discloses an ESG rating to third parties, the fund manager will have to include specific disclosures under the ESG Ratings Regulation on its website. The fund manager must also include a link to the website disclosures in those marketing communications. The ESG Ratings Regulation defines ESG rating.

Fund managers should examine marketing materials to establish if they disclose an ESG rating which triggers compliance with the ESG Ratings Regulation website disclosure rule by 2 July 2026.

Background

Regulation 2024/3005 on the transparency and integrity of ESG rating activities, (ESG Ratings Regulation), is designed to ensure that investors and other stakeholders have access to reliable and comparable information about ESG ratings’ objectives (what they assess) and methodologies (how they assess). ESG ratings are mainly developed and distributed by specialised ESG rating providers, however, some financial institutions also develop their own ESG ratings.

The ESG Ratings Regulation regulates the provision of ESG ratings in the European Union by entities who issue, publish and distribute ESG ratings on a professional basis (ESG Ratings providers). ESG Ratings providers operating in the EU will need to be authorised by ESMA to do so and comply with specific organisational and governance requirements.

ESG Ratings providers must also disclose to the public, on their website, methodologies, models and key rating assumptions used in ESG rating activities. They must also disclose specific information to users of ESG ratings, rated items and issuers of rated items. The content of these disclosures is prescribed in Annex III to the ESG Ratings Regulation.

UCITS managers and AIFMs which disclose an ESG rating to third parties as part of marketing communications are also subject to the Annex III disclosures but limited to the ‘minimum disclosures to the public’ set out at point 1 of Annex III. The ESG Ratings Regulation also amends SFDR marketing communication rules and applies equivalent disclosure obligations to entities in scope of SFDR which disclose an ESG rating to third parties as part of marketing communications. To avoid duplication of disclosures, fund managers may have regard to already published information in determining their disclosure obligations under the ESG Ratings Regulation.

The ESG Ratings Regulation entered into force on 1 January 2025 and becomes effective on 2 July 2026.

What is an ESG rating?

The ESG Ratings Regulation has a specific definition of ESG rating. It means an opinion or score, or combination, regarding a rated item’s profile or characteristics or exposure to risks or impact with regard to environmental, social and human rights, or governance factors that is based on both an established methodology and a defined ranking system of rating categories, irrespective of whether such ESG rating is labelled as ‘ESG rating’, ‘ESG opinion’ or ‘ESG score’.

There are also specific definitions of “ESG opinion”, “ESG score” and “rated item”.

Fund managers may reference ESG ratings or assessments in marketing communications for several reasons and in different ways. They may be proprietary ESG assessments or third party ESG ratings and may refer to a specific portfolio position or be at aggregate level. Consequently, there has been debate across industry as to what exactly can be regarded as “disclosing an ESG rating as part of its marketing communications” in accordance with the definitions in the ESG Ratings Regulation.

Careful analysis may be required to establish if an “ESG rating” within the meaning of the ESG Ratings Regulation has been disclosed and if it is used in such a way in a marketing communication to trigger the ESG Ratings Regulation disclosure rule.

Note that the ESG Ratings Regulation does not apply to specific mandatory disclosures under SFDR, such as pre-contractual and periodic disclosures.

Marketing communications

There is no definition of “marketing communications” in the ESG Ratings Regulation. There has been discussion at industry level as to what is an appropriate reference for fund managers to determine what constitutes marketing communications for the purpose of the ESG Ratings Regulation disclosure rule including use of the ESMA Guidelines on marketing communications under the Cross-Border Distribution of Funds Regulation. Each fund manager should assess what fund materials should be categorised as marketing communications for this purpose.

Website disclosure

ESG Ratings providers are required to disclose information on their website such as an overview of rating methodologies used, an overview of data sources, the ESG rating’s scope and the weighting of the E, S and G component of aggregated ESG ratings.

Fund managers subject to the ESG Ratings Regulation disclosure rule are required to make the same website disclosures as those required of ESG Ratings providers under point 1 of Annex III to the ESG Ratings Regulation.

This website disclosure is designed with ESG Ratings providers in mind, not fund managers, and is specific to how an ESG Ratings provider operates. For example, disclosure is required about the ownership structure of the ESG Ratings provider.

This means that where a fund manager concludes that the use of ESG ratings in its marketing communications does in fact trigger the ESG Ratings Regulation disclosure rule, compliance with the prescribed website disclosure content is not straightforward. In addition, the regulatory technical standards which are to be produced by the European Supervisory Authorities to specify the website disclosure information for fund managers under SFDR are on a European Commission list of de-prioritised level 2 measures and so will not be available before 2 July 2026. These RTS are to take account of information already disclosed pursuant to SFDR website disclosures.

Key issues for fund managers to consider

If you would like support to review marketing materials to assess whether the ESG Ratings Regulation disclosure rule applies, to draft website disclosure or general advice in relation to these matters please contact any of our Asset Management & Investment Funds Partners or your usual contact at William Fry.