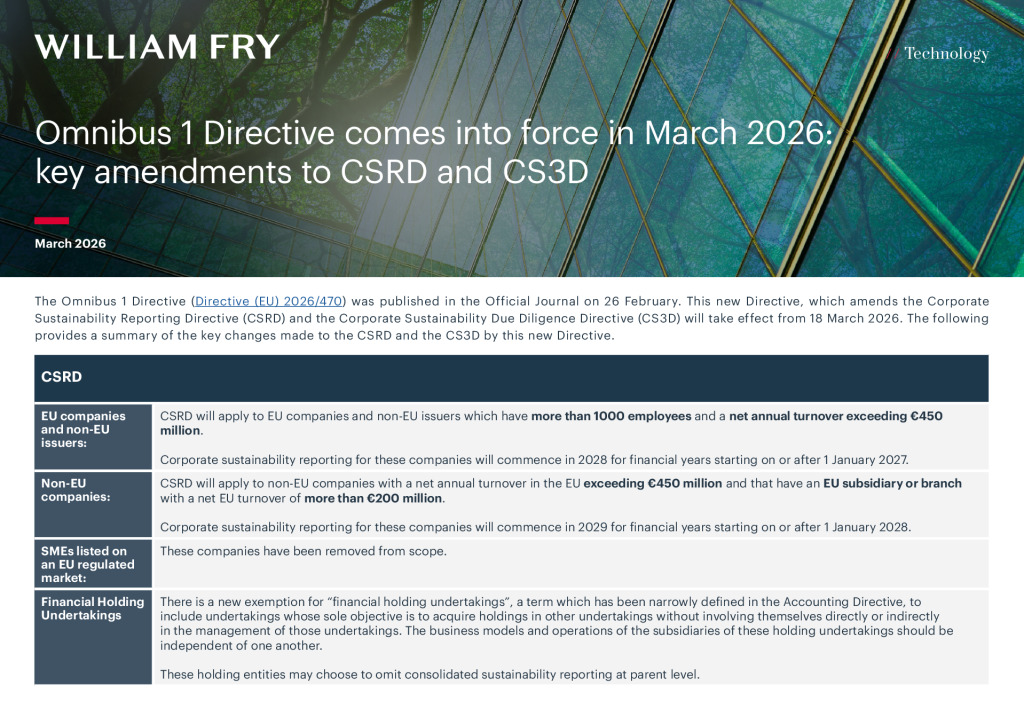

The Omnibus 1 Directive (EU) 2026/470 (Omnibus 1 Directive) was published in the Official Journal on 26 February.

This new Directive, which amends the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CS3D) and related Directives including the EU Accounting Directive, will take effect from 18 March 2026 (20 days after publication).

Member states will have 12 months until 19 March 2027 to transpose the Omnibus 1 Directive to the extent that it deals with amendments to the CSRD and related Directives. The transposition deadline for amendments to CS3D is 26 July 2028. In-scope companies will be required to comply with the new requirements of CS3D from 26 July 2029.

CSRD and CS3D have been substantially amended with changes made to significantly reduce their scope and the level of reporting obligations under them. Only the largest companies and groups will now fall under CSRD for mandatory corporate sustainability reporting and under CS3D for sustainability due diligence. It is estimated that approximately 80% of companies have been taken out of the scope of CSRD and CS3D by this Directive.

The overview table below highlights the key amendments made to the CSRD and the CS3D by the Omnibus 1 Directive.

What do these changes mean for Irish companies?

The companies caught within the scope for sustainability reporting under CSRD in 2025 for FY2024 will need to assess whether they remain within scope. According to a recent IAASA report (link here), only 20 Irish companies were required to report for FY 2024 under the Irish Corporate Sustainability Reporting (CSR) Regulations. The majority of these “wave 1” companies are likely to remain within scope and will continue to report in 2026 and beyond as part of their corporate sustainability reporting obligations under CSRD.

In relation to those “wave 1” companies which will fall out of scope when the Omnibus 1 Directive has been transposed into Irish law, the transposing Irish Regulations may exempt these companies from corporate sustainability reporting in 2026 and 2027 on FY 2025 and FY 2026 respectively and beyond.

How quickly the Department of Enterprise, Tourism and Employment can turn around new Regulations to transpose these amendments will determine whether out-of-scope wave 1 companies, will be exempted from reporting under CSRD in 2026 and 2027.

The simplification of the ESRS, including the forthcoming Delegated Act to be adopted by the Commission, will determine future reporting requirements for in-scope companies.

The concept of “wave 2” and “wave 3” companies for corporate sustainability reporting purposes has fallen away as a result of the changes made by the Omnibus 1 Directive. SMEs listed on an EU regulated market have been removed from scope and many “large” Irish companies which were initially within scope (under the old thresholds) are no longer in scope for mandatory reporting.

Any other very large Irish companies (whether listed or not) which meet the new thresholds (i.e. have over 1000 employees and a net turnover figure exceeding €450 million) but which were not caught for “wave 1” reporting, will be required to report under the new Irish CSR Reporting Regulations, once transposed. These companies will report in 2028 for FY 2027 going forward, When the new Irish Regulations are in place, Part 28 of the Companies Act 2014 on Sustainability Reporting will be amended to narrow its scope in line with the Omnibus 1 Directive.

Voluntary Reporting and keeping structured and transparent ESG data – why is this important?

Although the Omnibus 1 Directive has taken a significant percentage of companies out of scope for mandatory reporting under the CSRD, this does not mean that out-of-scope companies can close the book on sustainability reporting or on keeping clear and structured ESG information.

Having structured and transparent ESG data across operations and value chains will remain important for businesses to meet the requirements and expectations of customers, investors, lenders, and insurers.

Many Irish SMEs, that fall into the value chain of larger CSRD reporters, will be asked for structured ESG data. Tools like the voluntary reporting standards (VSME) developed by EFRAG can help to provide companies with a practical and standard way to record and report on their ESG information.

VSME provides a simple reporting tool for SMEs to deal with growing sustainability data requests from business partners and CSRD reporters. It also acts as a “shield” for SMEs as in-scope companies may not require information from business partners in the value chain that exceeds the content of the voluntary standard.

Next Steps

The Omnibus 1 Directive will take effect on 18 March 2026. Member states will have until 19 March 2027 to transpose the Omnibus 1 Directive to the extent that it deals with amendments to the CSRD and related Directives.

The transposition deadline for amendments to CS3D is 26 July 2028. In-scope companies will be required to comply with the new requirements of CS3D from 26 July 2029.

Click on the document below to download a summary of the key changes to CSRD and CS3D.

Contributed by Tracy MacDevitt